Over the last year, Embracer has made significant progress in shaping the future of the Group. We have improved the balance between growth and cash flow generation. The divestments of parts of Saber Interactive and Gearbox Entertainment will improve profit margins and cash conversion, and reduce financial leverage, while the subsequent intention to initiate a separation of the group into three separate publicly listed companies, sets a clear strategic direction. For the full year, excluding the contribution from the divested assets, we reached Net sales of SEK 39.7 billion, Adjusted EBIT of over SEK 7.3 billion and EBITDAC of SEK 6.3 billion on a pro forma basis.

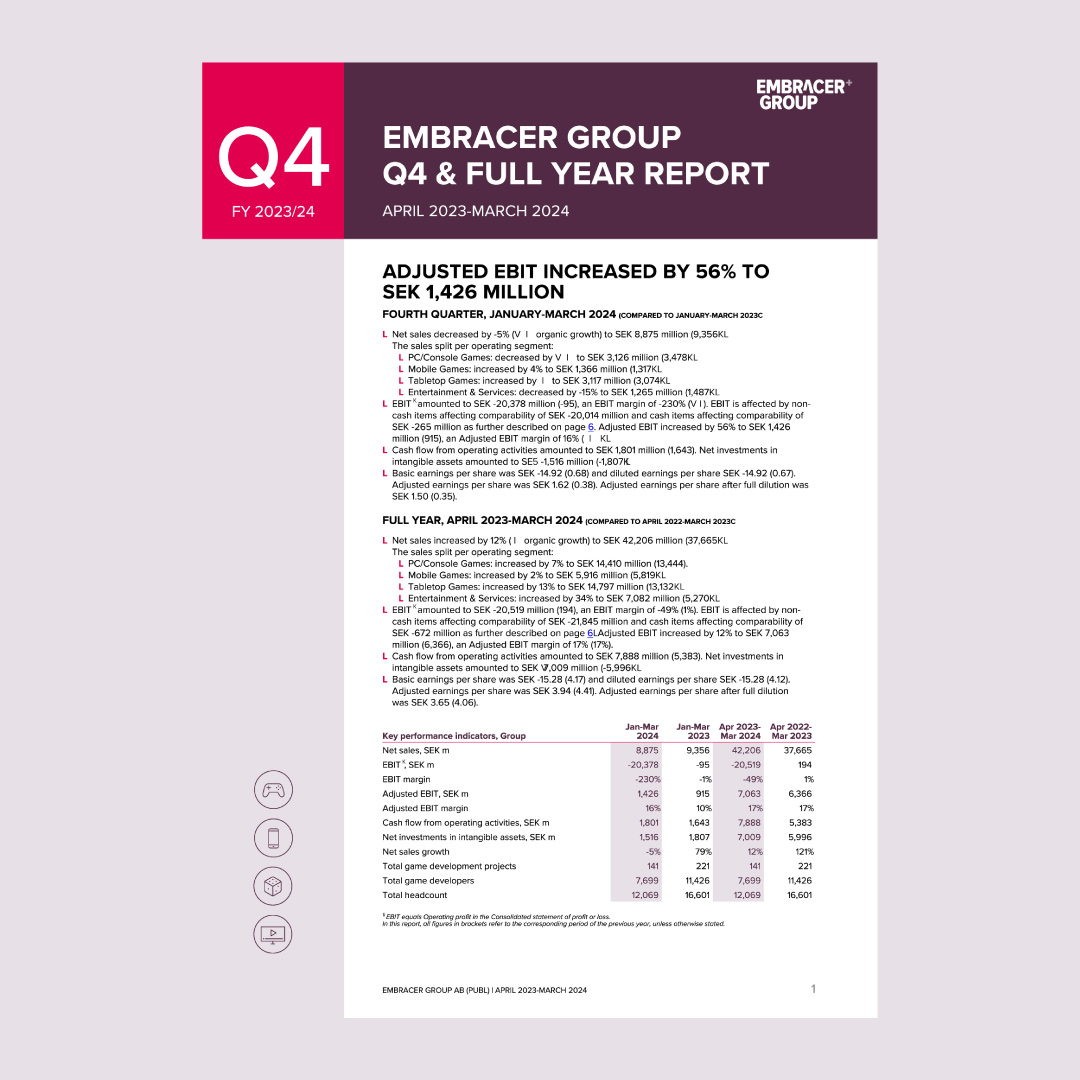

In the quarter, Embracer’s reported net sales, including divested assets, decreased by -5% YoY to SEK 8.9 billion. Organic growth amounted to -10%, negatively impacted by Entertainment & Services and a soft performance for the recently divested assets within PC/Console Games. Profitability notably improved in Q4, with an Adjusted EBIT of around SEK 1.4 billion, up by 56% YoY.

Free cash flow also materially improved YoY, to around SEK 0.5 billion, despite a negative EBITDAC contribution of SEK 0.5 billion from the divested assets in the quarter. For the full year, free cash flow amounted to SEK 1.5 billion, despite a negative EBITDAC contribution of SEK 2.2 billion from divested assets. This marks a strong improvement versus FY 2022/23, when free cash flow amounted to SEK -39 million.

A range of items not affecting cash flow had a SEK 20 billion impact on our reported EBIT in Q4, mainly relating to the actions we have recently taken. Approximately SEK 11.4 billion is related to the divestments of assets from Saber and Gearbox, and SEK 1.0 billion is related to the restructuring program. The annual impairment test also resulted in a SEK 6.7 billion impairment for Asmodee, which equates to around 20% of the SEK 34.4 billion consideration in 2021. Asmodee is still expected to generate mid-single digit organic growth in addition to any acquisitive growth, with an expanding Adjusted EBIT margin in the coming years. In Q4, the cash effect of the restructuring program amounted to SEK 265 million.

FY 2024/25 is expected to provide a similar performance on a like-for-like group basis compared to the actual Adjusted EBIT in FY 2023/24, with materially improved free cash flow and EBITDAC. There is potential for earnings growth across PC/Console, Tabletop and Mobile, with higher predictability within Tabletop and Mobile. Entertainment & Services is likely to have a somewhat lower profit YoY due to tough comparisons and a somewhat lower expected contribution YoY from Middle-earth Enterprises. A key assumption for our view of the year is that two key releases, Kingdom Come: Deliverance II and Killing Floor 3, within PC/Console, will reach the market successfully, largely in line with Dead Island 2 and Remnant II in FY 2023/24. In total, we expect to release more than 70 projects in FY 2024/25, including at least three important unannounced titles. Beyond FY 2024/25, we continue to see strong growth potential from a higher number of large-sized PC/Console projects, based on both established and new IPs.

In Q1, we expect a broadly stable Adjusted EBIT development YoY for Mobile Games and Tabletop Games, but a limited Adjusted EBIT contribution for both Entertainment & Services and PC/Console, due to the timing of new product releases. The value of completed games development within PC/Console is currently expected to reach around SEK 3.9 billion in FY 2024/25, of which approximately 10% in Q1, 20% in Q2, 55% in Q3 and 15% in Q4.

Solid earnings progression across key segments in Q4

In the PC/Console Games segment, we saw negative organic growth of -13% in the quarter, mainly explained by a soft performance for divested assets, with tough comparisons from a high contribution from deals signed by Saber Interactive in Q4 last year. The pro forma growth in the quarter was 3%, excluding divested assets. The quarter saw several small- and mid-sized new game releases, which supported growth. Overall, a few titles, including Tomb Raider I-III Remastered and Deep Rock Galactic: Survivor performed well. Meanwhile, a few mid-sized titles from THQ Nordic saw a more mixed performance. The Adjusted EBIT grew by around 50% YoY in Q4 due to easy comparison figures from last year. The 16% margin remained impacted by a relatively low return on investments (ROI) for primarily small-and-mid-sized releases in the past 18 months.

We remain excited about our PC/Console pipeline over the coming years. Our resources within PC/Console are increasingly focused towards our own and controlled key IPs, such as Darksiders, Dead Island, Deep Rock Galactic, Kingdom Come: Deliverance, Killing Floor, The Lord of the Rings, Metro, Remnant, Satisfactory, Tomb Raider, Wreckfest and many others. Through this year and next, we expect our updated capital allocation process, with improved standards for new and continued investment, to drive improving ROI from new game releases, as our pipeline increasingly consists of higher quality games.

In the Tabletop Games segment, Adjusted EBIT grew by over 50% YoY to SEK 380 million in Q4, with a notably improved margin YoY supported by a better product mix and a free cash flow above 100% of Adjusted EBIT in the full year. The organic growth amounted to -3% in the quarter and 7% for the full year. Growth was supported by the successful launch of Star Wars: Unlimited, offset by other trading card games due to release timings. Upon release of the first set for Star Wars: Unlimited – Spark of Rebellion, demand notably outpaced supply. Set 2, Shadows of the Galaxy, will be released on July 12th and Set 3, Twilight of the Republic, in the last quarter of calendar 2024. Asmodee, together with the renowned internal studio Fantasy Flight Games, has a clear multi-year roadmap with product development for several future sets already finished and remains focused on creating a strong ecosystem for players and retailers to install Star Wars: Unlimited as a long-term success. Further ahead, we also look forward to the release of the Altered trading card game in September this year.

The Mobile Games segment had another strong quarter, with over 50% Adjusted EBIT growth YoY to SEK 514 million. The Adjusted EBIT margin came in at 38%, with stronger-than-expected profitability driven by a product mix shift towards more hardcore games, lower user acquisition costs and an optimization of the balance between current and future potential profits. The organic growth amounted to -9% in the quarter and was in line with the FY 23/24 outlook. Easybrain continues to perform strongly, with high single-digit organic growth, while DECA Games saw negative organic growth, but with improved profitability and cash flows.

The Entertainment & Services segment had a quieter quarter, as expected, with fewer new releases and products compared to previous quarters, both for PLAION Partner Publishing & Film and for Middle-earth Enterprises. Organic growth amounted to -18% and the Adjusted EBIT margin was stable YoY at around 4%. After the quarter, Middle-earth Enterprises could finally confirm that two new films from Tolkien’s Middle-earth are in the works and, separately, Crystal Dynamics announced a new partnership to create new films and TV series for Tomb Raider.

We see great potential in The Lord of the Rings IP and believe the universe can become a key driver in the coming decades, with the aim to delight fans across the globe. New Tomb Raider stories in streaming and film will allow us to further nurture and grow another unique IP, taking it to new heights. Strong partners, such as Warner Bros. Discovery and Amazon MGM Studios, that complement our capabilities are an important part of our IP strategy.

New chapter to drive value across the business

It has been a transformative year for Embracer. The restructuring program, that is now successfully finalized, has created a stronger foundation for improved profitability, cash flows and long-term value creation. We are now at a capex run-rate of around SEK 4.3 billion as of Q4 on a pro forma basis. We are also on a path towards significant net debt reduction, driven by cash inflows from divestments and improved free cash flow.

Throughout the past year, our companies and studios have had to part ways with team members. These were necessary but difficult decisions, and it has been important to carry out the changes with compassion, respect and integrity towards those affected. Post-restructuring, we will strive to make continuous improvements as part of our ordinary business, to further improve operational efficiency and capital allocation.

As announced on April 22, we have initiated the process to separate into three separate, publicly listed entities. It is encouraging that shareholders share our view of the transformational separation. So far, the processes are tracking according to plan. There is significant untapped potential within the group, which I am confident the new structure will unleash. Asmodee, “Coffee Stain & Friends” and “Middle-earth Enterprises & Friends” will all boast sufficient scale, coherent strategies and a clearer focus, paving the way to unlock value in our high-quality assets. Importantly, each standalone entity will ultimately be able to fully utilize its own balance sheet, its own set of financial targets and optimal financing structure and capital allocation strategy that enable their growth ambitions. This, in turn, will create value for all stakeholders as it notably improves the conditions for our entrepreneurs and employees to create the best possible games.

We are now starting a new and exciting chapter for the businesses and people that make up Embracer Group. I am excited about the future and fully convinced that the best is still ahead of us. To conclude, I would like to send my thanks to all our team members, shareholders, customers, and business partners for contributing to the continued prosperity and success in our new chapter.

May 23, 2024, Karlstad, Värmland, Sweden

Lars Wingefors

Co-founder & Group CEO

Solid earnings and cash flow momentum in Q4 as new chapter is set to begin

In Q4, we delivered Net sales of SEK 8.9 billion and a strong improvement in both earnings and cash flows. Adjusted EBIT grew by 56% YoY to SEK 1.4 billion with a free cash flow of SEK 0.5 billion, despite a negative SEK 0.5 billion EBITDAC contribution from divested assets. Mobile Games saw continued strong earnings momentum and Asmodee successfully released Star Wars™: Unlimited, building a strong foundation for the continued roll-out plan of the game. We expect a similar Adjusted EBIT performance in FY 2024/25 as in the past financial year with a materially improved free cash flow and EBITDAC. The restructuring program is now successfully finalized as of 31 March and the processes to transform into three separate publicly listed companies are tracking according to plan.