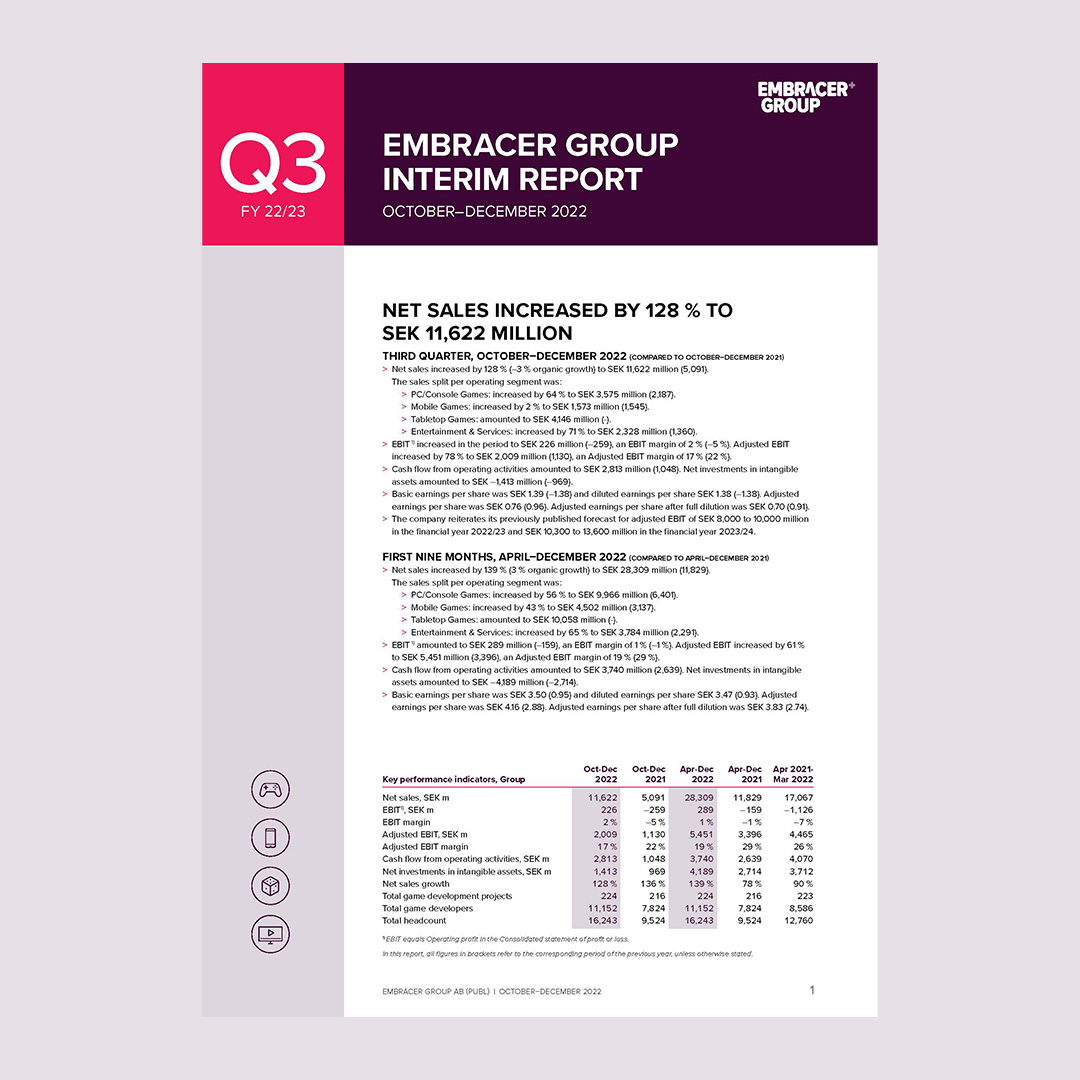

The organic growth in Q3 of –3 % reflects tough year-on-year comparisons and limited new PC/Console game releases. Adjusted EBIT came in at SEK 2 billion in the quarter despite limited contribution from content partnership deals, while free cash flow during the quarter improved to SEK 1.7 billion, exceeding management expectations.

For the overall group, we reiterate our Adjusted EBIT forecast of SEK 8.0-10.0 billion in FY 2022/23 and SEK 10.3-13.6 billion for FY 2023/24. We see a continued stable performance for live game services and for our strongest PC/console franchises, but also note a more normalized market for certain categories, partly due to softer consumer purchasing power, after a strong market both in 2020 and 2021. As previously communicated, the forecast includes a notable range of outcomes from partnership and licensing deals with several industry partners expected to be completed during the financial year 2022/23. In the Mobile Games segment, we expect seasonally lower activity and ad prices in Q4. In the Tabletop Games segment, we expect the seasonally lowest activity and Adjusted EBIT margin of the financial year, in line with historical patterns.

Diversification provides stability

Our business has grown increasingly diversified in recent years, adding stability to our results and cash flows. In the PC/Console Games segment, Coffee Stain successfully released Goat Simulator 3 to strong acclaim from fans providing a platform to further grow the player base over time. Together with our Danish colleagues at Ghost Ship Games, who continue their impressive work with Deep Rock Galactic, there is a lot to look forward to from Coffee Stain going forward.

That said, delays announced in previous quarters have led to a limited number of large-budget game releases for the PC/Console Games segment and a lower gross profit contribution in FY 22/23, impacting operating margins. The profitability in PC/Console in Q3 is also impacted by the amortization of game development costs for titles released with a lower ROI in Q1 and Q2, including the Saints Row reboot. It is a fact that certain operative groups in our PC/Console Games segment

have underperformed our expectations this year, largely driven by a sub-par ROI for its new game releases.

Rather than a structural shift, we believe it is mainly an effect of mixed reception for several releases, combined with a more normalized market and softer consumer purchasing power this year. Our core business is making a healthy risk-adjusted profit on games. We have therefore increased management focus and efforts to optimize investments and efficiency across the group even further. To simplify, each project has to earn its right to exist, which means we will increase our efforts to put quality first even further, and make sure we create unique positive player experiences.

I am confident that the impact of these factors will be short-term, as the group now gears up for an increasing number of notable releases within PC/Console from several studios and established IP with strong historical track records. After assessing our pipeline, we are confident in clearly improved ROI on new products compared to the last quarters. PLAION is approaching the release of the anticipated first-person action RPG Dead Island 2 on April 21. Several other upcoming large-budget games have also recently been announced for FY 23/24, including Warhammer 40,000: Space Marine 2, Remnant 2, and Payday 3. In total, we have 94 projects scheduled to be released FY 23/24 of which 58 are yet to be announced. We have invested significantly in one of the most diversified pipelines in the industry, empowered by the combined force of more than 11,000 game developers across the globe. In total, we have SEK 8.2 billion invested in ongoing game development projects as of December 31, 2022. For context, we have 31 AAA games slated to be released by FY 2027/2028 including 19 games that will ship by FY 2025/2026.

Within the Tabletop segment, Asmodee delivered solid performance, driving strong sequential revenue and earnings growth, as well as stronger free cash flow, despite a challenging macro environment in the seasonally strongest quarter of the year. Asmodee is expected to deliver full-year earnings largely in line with expectations from last year, with significantly improved free cash flow in the second half of the year. In FY 2023/24, we expect a cash conversion above 100 % for Asmodee as the inventory fully normalizes.

In the Mobile Games segment, Easybrain and DECA Games have successfully optimized user acquisition investments, balancing organic and paid downloads. This has provided strong profitability and cash flow in the quarter. The quarter saw solid sequential growth, reflect- ing the positive seasonality effects. However, we also experienced some headwinds from tough comparisons and lower ad prices compared to last year, impacted by Apple’s changes related to IDFA, lower player engagement post-covid and macroeconomic factors. Our mobile gaming companies are expected to show continued profitable growth in the years ahead.

In the current financial environment, we have built our resilience and agility by maintaining a solid balance sheet. We expect to reach our financial leverage target by the end of this financial year with no material loans to expire prior to June 2024. Going forward, we will focus on further deleveraging our balance sheet while allowing for selective continued growth investments.

Targeting a better balance between growth, profits and free cash flow

Our investments have put Embracer in a strong position for organic growth in both earnings and free cash flow per share. It has also strengthened our position vis-à-vis platform owners and other industry partners, looking to increase their exposure to future releases of high-quality games.

Capitalizing on our collective value and realizing the full potential of the Embracer ecosystem remains a priority

for the Group. The demand for content has never been greater, and Embracer is well-positioned to leverage that demand with the largest portfolio of games and IP in the industry. We have set the goal to increase the mix of PC/Console games development that is wholly or partly funded by third parties. This mainly relates to a range of large-budget upcoming games over the coming six years. While a majority of the overall pipeline will still be wholly funded within the Group, expanding third-party funding is expected to significantly improve cash flow and profit predictability. The Tomb Raider agreement with Amazon that we entered into during Q3 is one example of this type of partnership and one of the deals with several industry partners, previously discussed in conjunction with our Q2 report, that is jointly transformative. Additional deals are expected to close during the financial year 2022/23.

To further strengthen our partnership approach, I am happy to welcome Careen Yapp to Embracer Group. In her new role as Chief Strategic Partnerships officer, Careen will be responsible for aligning strategic Group partnership objectives with each operative group to drive Group-wide results. With her broad industry knowledge and over twenty years of technology and entertainment experience, I know she will add significant value to Embracer Group’s ecosystem, shareholders and other stakeholders as we continue to leverage our collective strengths as a company.

Embracer Group has a diversified asset base with attractive market positions across multiple businesses in the gaming and entertainment industry. The board remains dedicated to ensuring that the Group is optimized to enable long-term value creation. The special review that was announced by the Board of Directors in our Q2 report in November is still ongoing. I want to be clear that our long-term strategy to support and empower entrepreneurs and creators remains unchanged.

Building on a solid foundation

In late December, we successfully changed the listing venue to Nasdaq Stockholm Main Market, further strengthening transparency, governance, and liquidity in our shares. The uplisting is a testament to the strong foundation we have built over the years.

A key part of our ongoing development and progress is an increased focus on sustainability, a priority area for me, the management, our businesses, and our people. It is encouraging to see that those efforts, and the strengthening of our corporate capabilities at the parent company, are paying off through improved ESG ratings. In the past few months, MSCI upgraded our ESG rating from BBB to A, and we are now also part of Sustainalyt- ics’ 2023 Top-Rated ESG Companies list.

To conclude, I would like to send my thanks to all our shareholders, employees, customers, industry colleagues, and business partners for contributing to the prosperity and success of Embracer Group.

February 16, 2023, Karlstad, Värmland, Sweden

Lars Wingefors

Co-founder & Group CEO

Stable quarter with improved free cash flow

We are pleased to announce another stable quarter for Embracer Group delivering largely in line with management expectations. Our diversified business mix across segments drove solid Net sales of SEK 11.6 billion, Adjusted EBIT of SEK 2.0 billion and SEK 1.7 billion of free cash flow in Q3 of FY 2022/23 despite a limited number of new game releases in our PC/Console segment.